Key Takeaways

- Real estate can support retirement planning through income, appreciation, and diversification.

- Rental income, equity growth, and inflation-adjusted rents are core value drivers.

- Risk management matters as much as returns when investing for retirement.

- Liquidity, maintenance, and market cycles should be evaluated upfront.

- Modern structures allow exposure to real estate without direct property ownership.

Disclaimer: The information provided in this guide is for educational purposes only and does not constitute financial, tax, or legal advice. Always consult with a licensed professional before making any financial or investment decisions.

Investing in real estate for retirement keeps showing up in serious conversations for a reason. It sits in that sweet spot between logic and leverage. You are not betting on vibes or chasing numbers on a screen. You are dealing with tangible holdings connected to things people will always need, like places to live, work, and do business.

That’s why many investors naturally pull real estate into a broader mix alongside equities, savings accounts, and other resources. When structured thoughtfully, including through professionally managed real estate platforms designed for long-term income, these holdings can support recurring inflows, long-term appreciation, and a kind of balance that helps portfolios stay upright when markets decide to get dramatic.

Let’s be clear, though. Real estate is not a cheat code. It’s not a shortcut, and it’s definitely not guaranteed. Like any allocation, it comes with uncertainty and trade-offs. The people who benefit most tend to approach it with patience, structure, and a long-term mindset instead of hype and shortcuts.

How Real Estate Can Support Retirement Income

Real estate can support later-stage inflows in a few different ways, which is why it keeps earning a seat at the table in long-term planning. The mechanics themselves are simple. The real advantage comes from how those mechanics stack consistently over time as part of real estate investing.

This is also where modern platforms like mogul enter the conversation. Built by former Goldman Sachs real estate executives, mogul offers fractional access to professionally vetted residential real estate, allowing investors to participate in income-producing properties without taking on the operational load of direct ownership. The focus stays on fundamentals, monthly distributions, real-time appreciation, and structures designed to keep investments separate and secure.

Before anything else, reliability matters.

What determines how reliable inflows from real estate are over time:

- How leases are structured and how often they renew

- Local supply and demand for rental housing

- Operating obligations and how well reserves are planned

- The quality and responsiveness of professional oversight

None of these are flashy, but they are the difference between steady performance and constant friction.

Monthly Income From Rental Activity

Rental holdings produce inflows through rent paid by occupants on a recurring schedule. That predictability is one of the biggest reasons real estate appeals to people who want dependable support for everyday expenses, especially when working with rental properties in established markets.

Once taxes, insurance, and general upkeep are accounted for, remaining inflows can complement other funding sources. For many investors, this layer supports retirement savings rather than attempting to replace every other asset they hold.

Long-Term Appreciation And Equity Growth

Beyond recurring inflows, real estate exposure can build ownership value as markets evolve. Appreciation does not move in a straight line, and timing always matters, but longer holding periods have historically supported value growth across many regions.

That accumulated value creates options later on. Some investors sell. Some refinance. Others restructure positions entirely. In certain situations, people liquidate select holdings or downsize exposure to rebalance principal as priorities shift. Flexibility is part of the appeal.

Inflation Sensitivity And Rent Adjustments

Real estate is often discussed as an inflation-aware allocation because rents tend to adjust over time. As operating obligations rise, inflows may increase as leases renew, helping preserve purchasing power in later years.

This dynamic differs from fixed-income instruments that quietly lose ground as prices climb. Rent adjustments are not automatic, though. They depend on demand, local conditions, and occupant affordability, which means outcomes vary by market.

Understanding The Risks Before You Invest

Let’s talk about the part everyone pretends doesn’t exist for the first five minutes of the conversation. Risk.

Every allocation has trade-offs, and real estate is no exception. Anyone telling you otherwise is either selling something or skipping the fine print. The upside is real, but so are the variables that shape performance over time. Understanding those variables is professionalism, not pessimism.

Vacancy And Tenant Turnover

Inflows depend on occupancy. When a unit is filled, things hum along. When it’s empty, inflows pause while obligations keep showing up right on schedule. That gap is not a surprise. It’s part of the deal.

Turnover adds another layer. Marketing, cleaning, and the occasional repair between leases all take coordination.

Factors that increase vacancy exposure include:

- Heavy concentration in a single area

- Pricing that runs ahead of local wage growth

- Seasonal demand patterns

- Loose screening or inconsistent enforcement

Smart planning assumes vacancies will happen instead of hoping they won’t.

Market Cycles And Value Changes

Markets move in cycles. Always have, always will.

Economic conditions, interest rates, employment trends, and regional demand influence values. Some periods are steady. Others stall or slide longer than expected, especially in areas facing population or job losses.

Spreading exposure across locations and holding types reduces reliance on any single market, but it never eliminates uncertainty entirely. Real estate rewards patience, not perfect timing.

Liquidity And Access To Capital

Real estate exposure is not instantly liquid. You cannot click a button and exit by lunchtime.

Selling takes time, and transaction friction can reduce net proceeds. For long-term planning, liquidity should be weighed alongside inflow potential.

Many investors balance real estate assets with more liquid holdings, so flexibility exists when life throws curveballs.

Direct Ownership As A Long-Term Strategy

Owning rental units outright remains one of the most traditional ways to allocate to real estate. Owning a rental property offers control, customization, and decision-making authority. It also comes with responsibility.

This approach works best for people comfortable making operational calls over long stretches of time.

Residential Versus Commercial Holdings

Residential holdings include single-family homes and small multifamily buildings. They are generally easier to understand, finance, and oversee, often involving a mortgage and long-term leverage. Most investors start here because the rules are familiar.

Commercial holdings involve offices, retail spaces, or industrial buildings. These typically operate under longer leases and represent a different type of investment. The upside can be attractive, but the complexity and capital requirements are higher.

Different tools. Different expectations.

Lifestyle Fit And Time Commitment Over Decades

Here’s the part that doesn’t show up in spreadsheets.

What feels manageable at one stage of life can feel heavy later. Coordinating maintenance, reviewing statements, responding to issues, or making decisions during market shifts all require attention. Some people enjoy that involvement. Others eventually decide their time is better spent elsewhere.

That’s why many investors reassess direct ownership periodically. The decision is rarely about performance alone. It’s about alignment with lifestyle priorities.

Real Estate Without Direct Ownership

Not everyone wants the keys, the calls, and the calendar invites.

For long-term planning, many people look for ways to allocate to real estate that reduce hands-on involvement while still offering exposure to inflows and appreciation.

Situations where indirect exposure may be more practical:

- When handling fixes or occupants no longer fit priorities

- When capital is spread across several goals

- When broader exposure is preferred over concentration

- When time availability matters more than control

This approach is often viewed as a way to diversify without managing daily operations.

Fractional Structures

Fractional real estate investing models allow participants to hold an interest in a holding without owning the entire building. Instead of concentrating capital in one location, exposure can be spread across multiple properties.

Professionally Structured Access

Professionally structured real estate removes the need for individual decision-making around leasing or coordination. Participants gain exposure to inflow-producing holdings while outsourcing day-to-day tasks.

For people who value time, simplicity, and clarity, this approach can align better than direct ownership while maintaining exposure to real estate holdings.

Real Estate Investment Trusts And Long-Term Planning

Real estate investment trusts, better known as REITs, are often the first stop for investors seeking exposure without owning physical holdings. They trade on public exchanges and hold portfolios of inflow-producing assets.

Their appeal is accessibility, liquidity, and simplicity. The trade-offs deserve attention.

How REITs Distribute Funds

REITs distribute funds to shareholders through dividends, usually sourced from rent collected across their holdings. Payments typically arrive quarterly.

Because REITs are publicly traded, share prices fluctuate alongside broader equity markets. Performance can be influenced by sentiment and interest rates rather than property-level fundamentals.

REITs Versus Direct Ownership

REITs offer liquidity and a built-in spread that direct ownership does not. Shares can be bought or sold quickly. However, the structure is not as advantageous as other models.

The trade-off is control and tax structure. Participants don’t make holding-level decisions, and dividends are generally taxed as ordinary income.

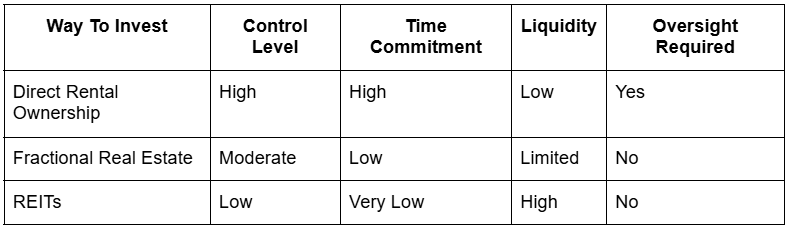

Comparing Different Ways To Invest In Real Estate

There isn’t one best way. There are only approaches that fit your goals and tolerance for involvement.

Key trade-offs are often weighed before choosing a structure:

- Control versus operational simplicity

- Liquidity needs versus long-term commitment

- Concentration exposure versus spread

- Personal involvement versus professional oversight

Choosing Platforms, Apps, And Structures For Real Estate In Retirement

These days, real estate doesn’t come in just one flavor. You’ve got options, and each one comes with a different level of control, effort, and long-term commitment.

Platforms Versus Funds In Retirement Planning

As more investors move past direct ownership and public REITs, the real question isn’t whether real estate belongs in retirement planning. It’s how you want to access it. Public REITs and real estate funds stay popular because they’re easy to buy, easy to sell, and familiar. The catch is that they move with the stock market and usually pay out quarterly, which can feel out of sync with how real-life expenses actually show up once the paychecks stop.

Why Real Estate Apps Have Gained Popularity

That disconnect is why real estate apps started getting real attention. These platforms are built for investors who want to browse deals on their phone, understand how properties are run, and collect income without fielding calls about leaky faucets. The best ones keep things clean: clear underwriting, simple onboarding, and reporting that helps you think in years, not trading days.

How Fractional Platforms Fit Between REITs And Ownership

Fractional real estate lives in the middle lane. Not full landlord mode, not stock-market roulette either. Instead of tossing everything into one big pool, these platforms offer property-level exposure while professionals handle the heavy lifting. Platforms like mogul tend to attract investors who want real estate to act like real estate, with recurring income and long-term alignment, without turning retirement planning into a second job. It’s not about chasing trends. It’s about choosing a structure that still makes sense when the goal is freedom, not busywork.

How Real Estate Fits Into Long-Term Retirement Planning

Retirement planning isn’t about predicting the future. If it were, we’d all be retired on private islands by now. It’s about building something sturdy enough to hold up when life does what it always does and changes the script.

Markets swing. Costs creep. Priorities shift. Real estate earns its seat in long-term planning because it operates in the real world, not just inside dashboards and forecasts. People still need places to live. Businesses still need space. That demand doesn’t disappear just because markets get noisy.

This is why real estate often acts as a stabilizer alongside equities and savings. Property-based exposure behaves differently from stocks, which can help smooth volatility over time. Diversification does not eliminate uncertainty, but it limits how much influence any single outcome has over the entire plan.

The goal is not to predict every move. It is to stay flexible, resilient, and positioned to adapt as life evolves. That’s not hype. That’s just playing the long game well.

Income Timing And Retirement Spend-Down Strategy

Here’s where things get practical.

Retirement expenses don’t arrive quarterly like dividends or once a year like a bonus. They show up monthly. Rent. Utilities. Food. Insurance. Life. Real estate inflows tend to match that rhythm better than most assets designed purely for growth.

That alignment matters.

Instead of forcing withdrawals at the wrong time, many investors use real estate to help cover baseline expenses, so other assets can stay invested longer. It’s less about squeezing every dollar and more about keeping the machine running smoothly.

People often ask themselves:

- Can inflows cover my core monthly expenses?

- How do these inflows behave when equity markets wobble?

- Do they adjust as inflation creeps in?

- What flexibility do I have if my needs change?

This isn’t about replacing everything else. It’s about giving your plan a backbone.

Tax Structure And Account Placement Considerations

Where real estate lives inside your financial life matters just as much as owning it in the first place.

Some investors look at real estate exposure alongside retirement savings vehicles like an IRA or a self-directed IRA. Others hold exposure in taxable accounts because they want access to inflows now, not later. There’s no universal playbook. There’s only alignment.

What people actually weigh looks more like this:

- How do distributions interact with my other income?

- Does depreciation or special tax treatment apply?

- Do holding periods line up with my retirement timeline?

- Can I adjust positions without creating unnecessary friction?

This is long-game thinking. Not optimization for a single year, but consistency over decades.

Risk Management Over Multiple Decades

Risk doesn’t retire when you do. It just changes outfits.

Early on, risk feels like volatility. Later, it looks more like inflation, sequence risk, or slowly watching purchasing power erode. Real estate plays defense differently depending on where you are in that timeline.

Over long horizons, most investors stop obsessing over short-term price moves and start caring about sturdier questions:

- Are inflows steady?

- Is demand durable?

- Can this hold its ground as costs rise?

- Do I have room to rebalance without being forced into bad decisions?

Diversification is the quiet hero here. Spread across locations and structures, real estate tends to absorb shocks instead of amplifying them.

Real Estate As A Tool, Not An Identity

The strongest investors don’t turn real estate into a personality trait.

It’s not about being “a landlord” or “a deal person.” It’s about using the asset class intentionally. Sometimes that means owning directly. Sometimes it means letting professionals handle the heavy lifting. Sometimes it means scaling back entirely as life priorities change.

None of that is failure. It’s a strategy.

Real estate works best in retirement planning when it supports your lifestyle instead of complicating it. When it adds stability instead of stress. And when it fits into a plan designed to evolve, not one frozen in time.

That’s not hype. That’s just playing the long game well.

A Modern Way To Invest In Real Estate For Retirement

As long-term planning evolves, more investors are looking for ways to invest in real estate without carrying the operational load of direct ownership. That shift has fueled the rise of professionally structured, fractional models.

Platforms like mogul reflect this shift toward cleaner, more intentional real estate exposure. Rather than asking investors to source deals or manage properties, mogul provides access to professionally managed assets with transparent reporting and structures designed for alignment.

What separates modern fractional models from traditional ownership:

- Centralized underwriting instead of individual deal sourcing

- Built-in oversight rather than self-handling

- Broader exposure without large capital commitments

- Structured reporting at the holding level

Where Real Estate Earns Its Keep In Retirement

Real estate remains a popular way to invest for later years because it blends inflows, tangible backing, and long-term potential.

Investing in real estate for retirement works best when the approach is intentional, balanced, and built for sustainability rather than short-term wins. Thoughtful planning and consistency tend to outperform hype.

For those exploring modern ways to access property-based exposure, learning how fractional investing works can bring clarity without the operational burden of traditional ownership. Platforms like mogul offer a streamlined way to participate in professionally managed properties while staying focused on long-term goals. If you’re curious how fractional investing works in practice, explore current listings and see how modern real estate access is being redefined.

Disclaimer: The information provided in this guide is for educational purposes only and does not constitute financial, tax, or legal advice. Always consult with a licensed professional before making any financial or investment decisions.

Frequently Asked Questions

What Is The 7% Rule for Retirement?

The 7% rule is a guideline discussed around withdrawal rates rather than guaranteed outcomes. It suggests drawing a higher percentage from a portfolio each year, which can increase available funds but also raises the risk of depletion.

What Is The 2% Rule for Property?

The 2% rule screens rental properties by comparing the monthly rent to the purchase price. It does not account for leverage, financing terms, maintenance, taxes, or market conditions.

How Much Should I Invest To Get R10,000 Monthly?

There is no single number. Outcomes depend on structure, market conditions, costs, and management approach. Many focus on building diversified inflow sources consistently.

Can I Retire At 60 With 500k In Savings?

It depends on spending needs, lifestyle expectations, and additional income sources. Professional guidance can help evaluate scenarios realistically.