Key Takeaways

- Stocks and real estate each offer different trade-offs, including liquidity and growth versus tangible cash flow and tax advantages.

- Dividend-paying stocks offer easy access and automatic compounding through DRIP. Real estate can provide rent-based monthly distributions and depreciation benefits.

- Interest rates and inflation affect each asset class differently, so diversification can help blend stability and growth.

- Fractional platforms offer lower-cost access to professionally managed real estate, while brokerages enable diversified stock exposure.

- The best approach is the one aligned with personal goals, time availability, and long-term investment strategy.

Disclaimer: The information provided in this guide is for educational purposes only and does not constitute financial, tax, or legal advice. Always consult with a licensed professional before making financial or investment decisions.

What if you could build wealth while avoiding the usual financial anxiety that shows up like an unwanted calendar reminder? That is exactly why so many people find themselves comparing dividend-paying stocks and rental real estate. Both can put money in your pocket, both can build long-term wealth, and both have fans who swear their lane is the winning lane. The truth is more interesting. Stocks and real estate simply play different positions in your financial lineup, and each brings a different kind of strength depending on how you like to invest.

Dividend stocks move fast and let you adjust your strategy with a few clicks. Real estate moves more slowly but often hits harder, especially when you combine monthly rents with long-term appreciation through fractional real estate platforms that keep the experience hands-off. Taxes, interest rates, inflation, and your personal tolerance for financial noise all influence which asset feels like home. And honestly, many investors discover the sweet spot is not choosing sides, but blending both so your money works from more than one angle.

Many investors also compare these approaches to broader vehicles like index funds, exchange-traded funds, and mutual funds, since those offer simple, low-maintenance exposure without needing to evaluate every individual asset.

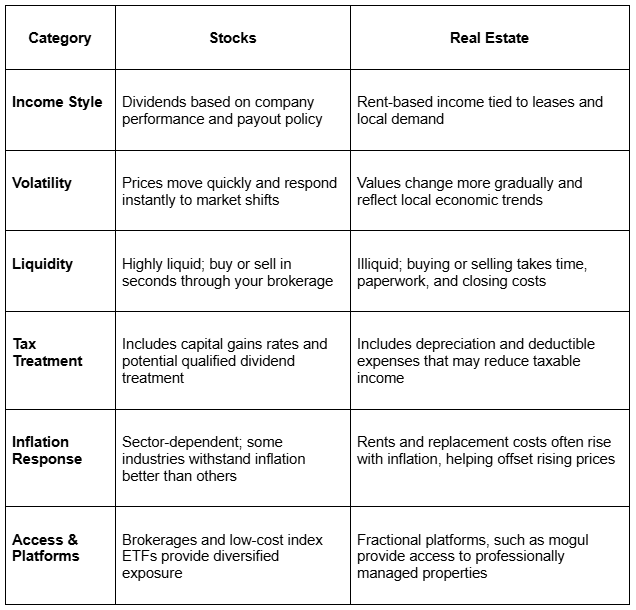

Income Stability and Cash Flow

Income stability matters when you want your investments to act like grown-ups. Rental income often does exactly that, showing up predictably when a property is leased. Dividends also bring income, but they depend on boardroom decisions and market cycles. One is a pre-planned monthly deposit. The other keeps you guessing just enough to stay humble.

Leases lock in income for a set period, and property managers help keep your day-to-day involvement to a minimum. Dividend payments arrive on preset schedules but sometimes change when companies face tighter margins. Each income stream has fans, but the reliability of either depends on how well you build your portfolio.

Real estate income often runs on multiple tracks at once, including rent, property appreciation, and principal reduction. Platforms like mogul, which offer fractional access to professionally managed properties, make it easier for investors to participate without the traditional hands-on responsibilities. Dividends rely on company profitability, sector performance, and earnings cycles.

Both can help build long-term wealth, but they behave differently when markets start moving in unexpected directions. Some people blend these income sources with real estate investment trusts, which distribute income without requiring direct ownership or property maintenance.

Dividend Payments from Stocks

Dividend investing is the definition of straightforward: you buy shares, and companies send you a portion of their profits. Fractional shares make it even easier to start with small amounts. DRIP programs do the heavy lifting by reinvesting payouts automatically. It is like having someone who keeps stacking the chairs for you while you talk to your friends.

Dividend stability depends on several factors. Some companies have decades-long streaks of paying and increasing dividends. Others cut payouts quickly during rough markets. A strong strategy focuses on sustainability rather than chasing the highest yields that look impressive but rarely stick around. Investors who prefer broader diversification often use dividend-focused index funds for steady income potential, avoiding the need to pick individual stocks or time the market.

Rental Income Predictability

Rental income is the more predictable sibling of the investing family. When demand is steady, leases keep the monthly cash flow flowing smoothly. Annual rent increases help maintain buying power. But even predictable income comes with fine print.

Vacancies, repairs, and shifting demand can change cash flow quickly. Some neighborhoods experience quick tenant turnover, while others are stable for years. And although hiring a property manager reduces daily headaches, it also takes a slice of your revenue. With the right planning, rental income can offer consistency that most stock investors envy.

Residential property and commercial property behave differently here, since each carries its own market risks, cost structures, and sensitivity to economic downturns.

Market Resilience by Property Type

A simple truth in real estate is that not all properties behave the same way. Some are steady performers that barely flinch during tough economic moments. Others are dramatic and need more attention.

Workforce and Multi-Family Stability

Workforce housing and multi-family assets often feel like the calm center of the storm. As long as people need places to live, demand tends to stay steady. Even during downturns, renters in essential housing markets usually stay put, which helps maintain occupancy and cash flow. Properties near transit, schools, and job centers often show the strongest consistency.

Niche and Short-Term Vulnerabilities

Short-term rentals and luxury homes tell a different story. Their performance depends on travel, leisure spending, and lifestyle demand. Any shift in tourism or local regulations can change income patterns quickly. These properties can deliver higher returns, but they need more attention, more dynamic pricing, and larger emergency funds.

Real Estate Versus Stock Market Returns Over Time

Both stocks and real estate can build wealth over decades, but they do it in very different ways. Stocks grow through price appreciation and dividends. Real estate delivers a layered return that includes cash flow, appreciation, loan amortization, and tax advantages. That mix creates a very different growth curve.

Stocks are also extremely liquid. You can buy or sell within seconds. Real estate takes patience, both in the buying process and in the eventual payoff. The upside is that real estate often rewards patience more generously, especially when combined with leverage that helps amplify returns. Unlike stocks, real estate is a physical asset tied to local demand, which is why everything from property taxes to mortgage interest can influence long-term returns more than national market movements.

Real Estate Return Components

Real estate returns often come from:

- Monthly rental income

- Appreciation over extended holding periods

- Principal reduction from mortgage payments

- Tax benefits, such as depreciation

Stocks provide capital gains and dividend income. Both require long-term commitment, but the timing, volatility, and structure of returns differ.

Historical Performance Comparison

Over many decades, disciplined stock market investors have seen strong long-term returns through compounding. But real estate plays a different game. Returns vary by location and property type, yet rental income and amortization create built-in value growth. Real estate also wins on stability, because price changes are gradual rather than minute-by-minute.

Transaction friction is higher in real estate. Closing costs, inspections, and longer timelines all add to the process. Still, many investors prefer real estate’s slow-and-steady rhythm to stock charts that jump like someone checking their phone notifications every 10 seconds.

Quick Side-by-Side Overview of Stocks vs Real Estate

Leverage Mechanics and Built-In Equity

Leverage can be a friend when used wisely, and real estate uses leverage differently than stocks do. Understanding the mechanics helps clarify why properties can produce impressive long-term returns even with modest appreciation.

How Mortgage Amortization Creates Value

A mortgage is like a financial treadmill that moves even when you do not. With every payment, more of your money goes toward principal instead of interest. Over time, this steady shift builds equity, whether property prices rise or fall. Investors who stay in the game long enough often see equity growth from amortization alone.

Contrast With Market-Driven Equity in Stocks

Stocks grow through market performance and investor contributions. There is no automatic repayment mechanism to force steady progress. Investors must stay disciplined to continue building exposure. Real estate, by contrast, grows equity simply by making payments on time, even during flat years. Direct ownership of an investment property also creates opportunities for higher market value over time, especially when mortgage debt is paid down consistently.

Impact of Interest Rates

Interest rates shape both investing paths, and they tend to do it loudly. Higher borrowing costs slow real estate demand and reduce affordability. Stocks can also react negatively because higher rates change how investors value future earnings. Rate cycles are among the biggest forces driving both markets.

Stock investing reacts differently, since higher rates often shift investors toward discount brokers, index funds, or employer-sponsored retirement account contributions when markets feel uncertain.

Rental income often remains more stable, even when interest rates climb. The cost of financing affects new purchases more than existing leases. Stocks show more immediate reaction, especially in growth-oriented sectors that depend on long-term projections.

Tactical Responses to Interest Rate Movements

Investors who understand rate cycles tend to stay calmer when markets shift. It is about knowing what to expect and how to position yourself.

Short-Term Tactics for Rising Rates

When rates spike quickly, it often makes sense to slow new acquisitions and secure fixed terms on existing loans. For real estate investors, this protects projected income and gives more predictability. Stock investors may reallocate their portfolios toward companies with stable earnings and less sensitivity to interest rates.

Opportunities During Falling Rates

Lower rates act like an energy drink for both markets. Real estate buyers can afford more, and refinancing becomes a way to lower payments and increase cash flow. Stocks typically see valuations rise when borrowing becomes cheaper. This is often when long-term investors rebalance or add to positions.

Tax Benefits and Implications

Taxes influence how much return you ultimately keep. Real estate offers depreciation and expense deductions that stock investors do not get. Stocks offer favorable long-term capital gains treatment for many taxpayers. Because tax rules vary, professional advice helps tailor the right strategy.

Real Estate Depreciation Advantages

Depreciation reduces taxable income even while a property appreciates. It does not change the cash flow you receive, but it changes how much you owe. The result is often a more efficient after-tax return profile for long-term investors. Investors also factor in tax deductions tied to real estate, particularly when comparing the long-term impact of depreciation versus capital gains treatment on stock investments.

Dividend Tax Treatment

Dividend tax rules depend on classification and holding periods. Qualified dividends usually receive better treatment. Certain dividends, such as REIT payouts, are taxed as ordinary income. Your after-tax yield depends on the type of dividend and the account you hold it in.

Volatility and Risk Factors

Risk shows up differently in real estate and stocks, and the experience of that risk matters. Stocks bring more immediate volatility because prices update constantly. Real estate pricing moves slowly, which can feel more stable even if the underlying risk is similar.

Diversification helps in both asset classes. Stocks reduce risk with broad index exposure. Real estate reduces risk through multiple properties or fractional portfolios. Liquidity is also a major difference. Stocks sell instantly. Real estate takes time and paperwork. Unlike real estate, which moves at a slower pace, stock markets can trigger panic selling, especially among investors who rely heavily on short-term news cycles.

Stock Market Fluctuations

Stock prices move daily based on earnings, economic news, and sentiment. If you watch too closely, the noise can be overwhelming. Dollar cost averaging helps investors stay disciplined by removing emotion from timing decisions. Unlike real estate, which moves at a slower pace, stock markets can trigger panic selling, especially among investors who rely heavily on short-term news cycles. Some investors spread exposure across mutual funds or exchange-traded funds to reduce the stress of monitoring individual companies.

Property Value Stability

Real estate values respond to local changes like job growth, school quality, and supply conditions. They move slowly enough to help investors avoid impulsive decisions. Unexpected repairs or market shifts can still impact returns, but the slower pace gives room to adapt. Investors seeking tangible assets often prefer this slower movement because it aligns better with long-term planning and reduces the pressure of daily price swings.

Practical Learning Paths and Resource Checklist

Learning how each asset works makes investing feel less like guesswork and more like a strategy.

Skills to Prioritize for Each Asset Class

Real estate investors benefit from understanding rent rolls, maintenance costs, and the quality of property management. Stock investors focus on reading financial indicators, dividend history, and payout sustainability. Both benefit from understanding how fees and taxes affect after-tax returns. Both approaches benefit from having a financial advisor or tax professional help interpret complex rules around retirement accounts and long-term planning.

Helpful Resources and Habits to Build

Small, consistent learning routines build confidence. Track one fund or one property for a quarter to see how reporting works. Subscribe to one solid housing report or one reliable earnings calendar. Simplicity beats overwhelm every time.

Inflation Protection Strategies

Inflation quietly chips away at buying power, so investors look for assets that keep up. Real estate often rises with inflation because replacement costs and rents increase. Stocks are mixed, depending on the sector.

Rental properties adjust to inflation through rent increases and rising property values. Stocks can hedge inflation when portfolios include industries that pass rising costs to consumers.

How Real Estate Hedges Inflation

Real estate offers multiple forms of inflation protection at once. Replacement costs rise, which pushes property values up. Rent increases help maintain income. Fixed-rate debt becomes cheaper in real terms.

Stock Performance During Inflation

Certain stock sectors handle inflation better. Materials, energy, and consumer staples often hold steady because they deal in essentials. Diversification helps even out the bumps.

Getting Started with Less Capital

Modern platforms have lowered the cost of entering both stock and real estate markets. Fractional shares make it easy to buy partial ownership in large companies or properties, and platforms like mogul give investors access to professionally managed real estate without taking on landlord responsibilities. This opens doors for investors who want diversification without massive upfront capital.

Some investors also experiment with buying stocks gradually through fractional shares, while others start small with investing in real estate through fractional or shared-ownership platforms.

Before investing, evaluate:

- Fee structures

- Transparency in reporting

- Asset selection and underwriting

- Liquidity options

Best Apps for Investing in Stocks and Real Estate

If you want the shortcut version of this debate, many investors compare platforms based on how easy they make life. For real estate, fractional platforms like mogul offer professionally managed properties, monthly distributions, and simple onboarding for people who prefer a hands-off experience. It turns real estate into something you can actually fit into a lunch break instead of a weekend renovation plan.

For stocks, your existing brokerage usually does the heavy lifting. Low-cost index ETFs give you diversified exposure with just a few taps, letting you build long-run stock growth without babysitting individual companies. Most brokerages also support fractional shares, which helps you build positions consistently over time.

The best app depends on how you like to invest. If you want real estate income without the headaches, fractional platforms make it easier to achieve. If you prefer liquidity and quick adjustments, brokerage platforms give you that flexibility.

Platforms That Make Income Investing Easier

Some investors prioritize steady distributions. Others want long-run market exposure that quietly compounds in the background. Fractional real estate platforms create predictable monthly distributions from professionally managed rentals. Everything from property oversight to tenant management is handled for you, which makes the experience feel intentionally simple.

Stocks create income differently. Dividend ETFs at your brokerage pay periodic dividends, and DRIP features reinvest those payouts automatically, helping your position grow over time. This approach gives you income potential, but with more price volatility because stocks respond instantly to market shifts.

Each method works in its own way. Real estate income tends to feel steadier because leases move slowly. Stock income feels more dynamic because markets change quickly. The right platform depends on how comfortable you are with those differences.

How Investors Rank Stocks vs Real Estate Platforms for Simplicity

When people compare the simplest ways to invest, a few patterns show up again and again. These are not recommendations, just common ways investors describe the experience when choosing where to start.

- Fractional real estate platforms

Many investors put these first for simplicity because they combine monthly distributions, appreciation potential, and professional management. The hands-off structure makes real estate feel accessible even for beginners.

- Brokerage platforms using broad index ETFs

Next on the list are low-cost index ETFs. They are liquid, diversified, and designed for long-run market exposure. Investors like them because you can buy or sell whenever you need to without extra complexity.

- Dividend-stock sleeves inside a brokerage account

Dividend stocks sit third on the list. They add income potential and DRIP-powered compounding, but require a bit more monitoring because payouts can change and individual companies behave differently.

These rankings are just one way investors compare simplicity. Your preferences and goals shape how each option feels in practice.

Fractional Real Estate Investing

Fractional investing lets you own a slice of professionally managed properties. This structure offers diversification and reduces operational risk. It provides access to markets that once required much larger commitments.

How mogul’s Platform Works

mogul gives investors fractional ownership of vetted properties, along with transparent reporting and a streamlined investing experience. The platform emphasizes monthly distributions, appreciation potential, and hands-off management. Investors can review current listings and educational materials at any time.

Practical Considerations When Choosing Between Stocks and Real Estate

Choosing between stocks and real estate depends on your goals, lifestyle, and tolerance for involvement. Stocks offer simplicity and immediate liquidity. Real estate provides income, tax benefits, and long-term stability. Many investors discover that combining both is the most balanced approach. What feels like a better investment often comes down to whether you prefer liquidity and instant pricing or the stability that comes from property ownership and rental income.

Your Next Step

Choosing an investment path is less about picking a winner and more about aligning with your goals, personality, and timeline. Stocks offer flexibility and instant liquidity. Real estate offers reliable income and tax advantages. Many investors choose to build a portfolio that can grow, withstand volatility, and support long-term goals. Exploring current listings on platforms such as mogul, or learning how fractional ownership works in general can help clarify which mix feels right for your financial strategy.

Disclaimer: The information provided in this guide is for educational purposes only and does not constitute financial, tax, or legal advice. Always consult with a licensed professional before making any financial or investment decisions.

Frequently Asked Questions

Which Is Better, Real Estate or Stocks?

Real estate provides rent-based income and tax advantages, while stocks offer long-term growth and liquidity. The better option depends on your financial goals, risk tolerance, and investing style.

What Makes More Millionaires, Real Estate or Stocks?

Real estate builds wealth through appreciation, rental income, and principal paydown. Stocks build wealth through compounding and broad market growth. Both can create millionaires when investors stay consistent.

Real estate investors with apartment complexes, mobile home parks, or strip malls see different risk profiles than those relying on individual homes, just as stock investors using index funds experience different outcomes than those betting on single companies.

What Is the 7 Percent Rule in Investing?

The term varies in meaning. Some traders use a seven percent stop loss, while long-term investors focus more on total return trends than on fixed percentage triggers.

How Do Dividend Stocks Compare to Rental Real Estate for Retirement Income?

Dividend stocks deliver liquidity and regular payouts. Rental real estate offers monthly rent and tax benefits. Both help build retirement income, but they differ in volatility and involvement. Some retirees blend these with real estate investment trusts to diversify income across markets.

How Do Interest Rates and Inflation Impact Real Estate Returns?

Higher rates increase borrowing costs and can slow buyer demand. Inflation raises rents and replacement costs. The combined effect depends on loan terms, location, and your holding timeline.